From the IMF comes a text on what demand for government debt can tell us about future risks of an economy. This basically means that the risk of potential default depends very much on who's holding the government debt, foreigners or domestic investors. Here is the paper, and this is their most interesting finding:

|

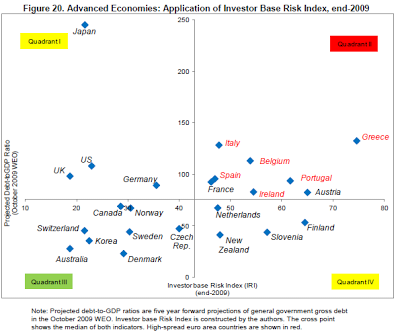

| Source: Arslanalp, Tsuda (2012): "Tracking Global Demand for Advanced Economy Government Debt", IMF working paper |

HT: The Economist

In Quadrant I we have countries with high debt but resilient to a run. In the second quadrant, we have countries with high debt and a high risk of a run (the worse combination). The third quadrant features countries with low debt and resilience to a run (the best combination), while in the fourth are countries with low debt, but prone to a run. The two measures used in designing the investor base index are the demand-side risk indicator (on the horizontal axis), and the supply-side risk indicator (on the vertical axis). And while the supply side indicator is simply a measure of debt-to-GDP, the demand-side indicator looks at ownership of debt (the investor base):

"By this metric, countries with a high share of domestic investors, such as domestic banks and central banks, as well as foreign central banks in their investor base receive lower scores. In contrast, we assign high scores to countries whose investor base has a high share of foreign private investors as we find they are the most skittish in times of trouble."

The findings are particularly interesting when observing them on a country by country basis, as is done in the graph. It tells us of the high riskiness of peripheral eurozone economies (rightfully including Belgium, but also France and Austria), and a worrying situation in the world's biggest economies of Japan, Germany, US and UK. Even though the later countries don't suffer directly from the risk of default, their high debt-to-GDP ratio makes them potentially risky, at least from the supply perspective. However, have in mind that the methodology of acquiring this data was to give low scores to countries whose debt is own mostly by domestic investors (as is the case with Japan, UK and USA). What this essentially implies is that all countries left of the vertical axis shouldn't worry about the sustainability of their debt since they have a lower risk exposure then their counterparts on the right of the axis. This is a dubious conclusion, as it would imply (from a game theoretical and political economy perspective) that all countries in the third quadrant should converge towards higher debt-to-GDP levels, which are apparently sustainable no matter how high they get, as the majority of debt owners are domestic households or investors. Why did I say political economy perspective? Because the governing politicians will find it more rewarding to run higher public debts to finance their concessions to various supporting interest groups. As long as the domestic entities are the ones barring the burden, there would be no reason for the government to stop this any time soon. Isn't this exactly the case of Japan?

On the other hand, any small open economy (which is basically every economy on the right side of the vertical axis except France) with greater exposure to foreign investments will never be able to run too high debt-to-GDP as their biggest constraint will be foreign ownership of government debt, and hence a higher risk of default. These countries will be (should be) converging towards the fourth quadrant. As a result we should end up with two types of countries; (1) those with high debt-to-GDP but with greater domestic ownership, thus making them less riskier (all the countries on the left do actually have lower bond yields than the countries on the right) and (2) those with low debt-to-GDP, where a constraint to higher debt levels will mainly be foreign ownership of debt.

I don't buy it. Even though their graph very precisely depicts the actual ratings on the sovereign debt market (except for France and Austria), the source of investment is not good enough of a category to differ between high and low risk countries. There is a multitude of other factors at work here. The Economist has a good explanation:

"There is no reason to think that domestic savers in the currency area are inherently less flighty than foreign ones. In previous currency crises, such as in Southeast Asia in 1997 and Argentina in the early 2000s, the first people to pull their money out were well-connected insiders rather than skittish foreigners. Something similar may have occurred in the euro zone. A Spaniard has very little reason to own Spanish government bonds rather than Dutch government bonds since both instruments are denominated in euros and both are ostensibly free of risk. However, if the Spaniard starts to think that a Spanish bond could be redenominated into pesetas, or could be written down as part of a “voluntary” “private sector initiative,” he has every reason in the world to swap his Spanish bonds for German or Dutch bonds—even if the risk seems vanishingly small. (In contrast, savers in countries with their own currency have to buy locally-denominated debt if they want to hedge long-duration fixed-income liabilities.)"